EMPIRICAL RESEARCH OF INVESTMENT POTENTIAL DRIVERS FOR ELECTRIC POWER INDUSTRY COMPANIES BY EXAMPLE OF PRICE-TO-BOOK VALUE RATIO

Кирьянова Е.С.

Студентка 4 курса, Высшая Школа Менеджмента, Санкт-Петербургский Государственный Университет

ЭМПИРИЧЕСКОЕ ИССЛЕДОВАНИЕ ДЕТЕРМИНАНТ ИНВЕСТИЦИОННОГО ПОТЕНЦИАЛА РОССИЙСКИХ КОМПАНИЙ ЭЛЕКТРОЭНЕРГЕТИЧЕСКОЙ ОТРАСЛИ НА ПРИМЕРЕ МУЛЬТИПЛИКАТОРА PRICE-TO-BOOK VALUE RATIO

Аннотация

В настоящей статье рассматривается определение наиболее адекватного показателя инвестиционного потенциала компаний электроэнергетической отрасли и выявление драйверов, оказывающих наиболее сильное влияние на индикатор Цена-Балансовая стоимость (MB Value, Price-To-Book Value Ratio).

Ключевые слова: эффективность деятельности, инвестиционный потенциал, инвестиционная привлекательность.

Kiryanova E.S.

4th year bachelor, Graduate School of Management, Saint-Petersburg State University

EMPIRICAL RESEARCH OF INVESTMENT POTENTIAL DRIVERS FOR ELECTRIC POWER INDUSTRY COMPANIES BY EXAMPLE OF PRICE-TO-BOOK VALUE RATIO

AbstractThe article comprises the determination of the most relevant company’s investment potential indicator and its application to Russian electric power industry, identification of most powerful drivers of Price-To-Book Value Ratio.

Keywords: performance measurement, effectiveness, investment potential.

Nowadays the problem of performance management of an organization is becoming increasingly topical, as for a modern company operating in a market economy and free competition it is crucial to be effective and competitive to exist in the market for a long period of time.

The objective of the research is to identify the germane indicator of companies’ effectiveness in terms of market value and attractiveness for investors. The main research problems are to analyze existing approaches of company’s performance management and by example of a certain industry, to consider Price-To-Book Value Ratio as a measure of shareholder value creation and determine its drivers.

Organizational effectiveness and performance measurement.

Effectiveness of the organization is not only important for enterprise owners who are interested in making profits, but also for all stakeholders of the company. Thus, company’s clients and suppliers, creditors and government agencies are interested in the solvency of the firm and regular payments from it in the state budget.

An effectiveness of a company implies actions to provide productive and cost-effective achievement of the objectives set for the organization. In other words, it is necessary to ensure such consistency of the company, its units, processes and employees, which would optimize the ratio of costs and desired results.

From the point of view of elements interaction in the economic system, organizational effectiveness can be considered as transformation of "contribution" of some stakeholders in the satisfaction of other stakeholders by achieving the desired results. Determination of the effectiveness level of the company is the way to identify problematic areas, inefficient departments, assessing the prospects for development of the organization, and, particularly, the level of achievement of its goals.

There are other important forms of performance of the company, such as product quality, speed of internal communication between departments, established business processes, motivated employees. And the most important task of modern management is to maintain the effectiveness of all the factors combined at a level that optimizes the organization activities, takes into account the interests of all stakeholders and minimizes costs.

But in order to manage the organizational effectiveness, it necessary has to be measurable. So, measurable and expressed in numerical terms indicators allow comparing of the obtained results with previous periods, with other departments or employees with other companies. Management decisions are based precisely on the idea of the current level of efficiency, awareness of the causes of the situation.

Causes of the current situation in the organization can be divided into internal and external. The external factors include the impact of the economic and political situation in the country, the level of competition in the industry, the national currency rate, reflected in the relative change in the volume of imports of foreign products, legislation to regulate the conditions of the company. These factors otherwise can be called unmanageable as individual agencies are not able to change their impact on efficiency.

Another group of factors can be called controlled or internal. These include corporate culture of the organization, its organizational structure, management principles, quality of resources used, the number of staff and a variety of other factors that may be specified for a particular industry. This group also includes indicators of labor efficiency and production assets, production profitability or productivity of a particular manufacturing plant. In other words, measurable performance indicators are the basis for management of the organization, and must be continuously monitored by management to improve organizational effectiveness.

In order to manage effectively each business process of the company, department and employee, companies establish quantifiable indicators of actual achievements - key performance indicators KPI, which reflect valuable information for managers.

In any organization the number of business processes is huge, and therefore, the number of key performance indicators is very large. Consequently, it is essential for management to establish a minimum limited set of the most important indicators for the organization.

Balanced Scorecard (BSC), the world widely used system developed by R. Kaplan and D. Norton, enables the integration of quantitative and qualitative indicators of business performance and helps build a causal relationship between the results and the impact of these factors results. Balanced Scorecard is a strategic approach to measure the effectiveness of the organization, establishing a set of long-term goals to achieve.

Review of existing performance measurement approaches for electric power industry companies.

Companies belonging to the electric power industry, as well as other international and Russian organizations, hold the view that today the ability to choose and prioritize the right measurable goals for the organization, to create a system to monitor them, and then effectively take managerial decisions is fundamental to compete in the market.

However, the introduction of KPI system, along with balanced scorecard system in Russia occurred relatively recently, and it, certainly, entailed benchmarking of systems already used by foreign organizations. Thus, most of the KPI in Russian and foreign companies are similar and are based on the financial statements.

Paramount for Russian companies are such indicators as operating profit in absolute terms (EBIT - Earnings Before Interest and Taxes), return on equity (ROE) and operating costs. The competitiveness of firms in the market is directly related to reducing transaction costs, and in Russia this figure is also used under the name "operating costs limit."

Alternatively, in international practice much attention is paid to the capitalization and financial sustainability of the company. Thus, it is important for companies to achieve a certain credit rating within the research of independent rating agencies such as Standard and Poor's, Moody's or Fitch Ratings. Rating indicates measure of creditworthiness of the company, so foreign companies are watching carefully at directly related indicators - the value of debt in absolute terms, the share of long-term debt in the company's total equity, the ratio of free cash flow to debt. Coming back to capital ratios, it should be said that the majority of foreign companies attach great importance to earnings per share as a crucial index for the shareholders of the company.

In Russia, the electric power sector is being in the last stage of reforming, and its development is directly connected with investments in various industrial projects. Therefore, great attention is paid to performance evaluation of such projects, which are aimed at the technical improvement and renovation of plant and equipment - net present value projects (NPV - Net Present Value), payback period (T) and return on investment (ROI).

The financial leverage, showing the relationship of debt to equity capital of the company is also taken into account by Russian companies and is included in the five most important performance indicators for "RusHydro".

The representative of the Institute of Social and Economic Research Center of the Russian Academy of Sciences, Gainanov I. D. considers the investment attractiveness of the modern Russian electric power industry companies as the basis for development in the current market conditions. From his point of view, the electric power industry reform does not contain decomposed targets for companies.

The author proposes the to use EVA (Economic Value Added) as a result of basic indicator of business performance, the growth of which can be achieved both by reducing the cost of capital and increase revenue or reduce operating costs.

However, the index of economic value added has a significant drawback: EVA reflects the profit for the current year, but not the future cash flows and their present value. For example, if a particular project requires substantial capital investment, for the first periods value of the index EVA is negative, even if the present value of future cash flows of the project is expected to be positive. Thus, the figure does not give an opportunity to evaluate the potential of the company.

Indicators of investment potential as the most relevant electricity industry KPIs

Today the main purpose of reforming is to provide investment flow into the sector for modernization and commissioning of new facilities in operation. So, at this stage of development of the industry the main problem is not just to attract investment, but also to improve the efficiency of investments by the company in its own assets at the expense of own and borrowed funds.

Value of the company, or its market capitalization, is the most important indicator of its effective operation, as it directly reflects investors' expectations regarding future growth in revenues and profits of the company. And the increase in capitalization, in its turn, shows the profitability and competitiveness of the enterprise, as well as its investment attractiveness, which is extremely important for Russian companies today.

In addition, for the shareholders dividend payments are very important, which is the main driver of investment attractiveness of electric power companies. Last thirty years for electric power companies from the developed countries it was typical to channel more a half of net profit to dividends. But to maintain the stability of dividend payments in absolute terms, in periods of lower net profit percentage was close to 100%.

For Russian companies of the industry is typical to direct almost entire net income on investments, return on which is often opaque for investors. So, today dividend yield of Russian electric power companies does not exceed 1.5%. But completion of the period of active growth, escorted by comparing Russian and European electricity prices and increasing risks of further reduction of income, leads to a rapid decrease in the capitalization of companies in the industry.

Particular attention should be paid to investment multiples that are market indicators, and therefore reflect the real investor expectations regarding the company's investment. Examples of cost multipliers may serve the following indicators: Market-To-Book Ratio (or Price-To-Book Ratio, Q-Tobin), Price-To-Earnings Ratio, Total Shareholder Return.

The coefficient P / E (Price-To-Earnings Ratio), which equals the ratio of the current market price per share and earnings per share, shows how many periods the investor must wait to fully compensate initial investment. Most investors pay great attention to this indicator, but it should be noted that the denominator of the multiplier is a profit derived using both own and borrowed funds, while the price reflects only the company's equity, and it is a big disadvantage of this index.

Cost multipliers are widely used in modern empirical research as they allow investors to determine the expected valuation of future super profits. In this connection it is necessary to consider in more detail the other multiplier reflecting the investment potential of the company.

Q-Tobin's, or Price-To-Book Value Ratio (P/BV, stocks security by balance-sheet assets) is the ratio of market capitalization value to its carrying value. The first advantage of index is its market nature: it shows how many units of currency investors are willing to pay per unit of currency invested in assets of the company. P/B Value shows the attitude of investors to the viability and feasibility of investment into a particular company. The market component is reflected in the numerator - the capitalization of the company equals the product of the company's stock price and the number of shares outstanding.

The denominator of the multiplicator reflects the carrying value of the company, which is defined as the difference between the value of all assets of the company and all of its liabilities. In other words, in the denominator reflects the company's net assets

So, Price-To-Book Ratio allows determining how the carrying value of the assets of the company is overvalued or undervalued by the market. If the indicator exceeds unity, this means a high attractiveness for investors. In other words, the company is able to effectively invest in its own assets, and therefore has a high investment potential and investors believe in its investment opportunities.

The attractiveness of this indicator in the study is also provided by its applicability to compare the performance of the company within the same industry. Because today in the Russian electric power sector there are many investment programs that require fundraising, the multiplier becomes important criterion for choosing the most potentially profitable ones.

Empirical Study: Determinants of shareholder value creation by Russian power industry companies

The next step is to identify the determinants of Price-To-Book Value Ratio for the Russian electric power companies, which characterizes their investment potential. Let us consider several empirical studies that will help identify the key factors influencing this multiplier.

Thus, the basis of my work is taken modern research, the results of which are shown in the electronic journal "Corporate Finance" in 2014, which means "fresh" approach to its implementation, as well as records of contemporary global trends in its development.

Based on the analysis of existing empirical studies [Bartov et al., 2002; Gou et al., 2005], the authors put forward a number considered determinants of shareholder value creation, which is represented by three groups of indicators: financial performance of companies, ownership structure and socio-economic and sectoral indicators

So, according to A. Kleidon research [Kleidon, 1986], the company's return on assets is a representative variable that explains a high proportion of changes in market share prices of companies. Economic profitability of activities that can also be interpreted as the return on assets was confirmed by investigations of I. Pandey in his empirical studies as a factor of the multiplier effect on the Price-to-book Ratio [Pandey, 2005]. In addition to the factor of return on assets, P. Chen and H. Zhang in their studies identified investment activity of companies and the dynamics of changes in profits as determinants of investment attractiveness of the company [Chen and Zhang, 2007].

Moreover, studies of famous scientists Fama and French showed that the size and age of the company are important factors in determining a company's ability to effectively invest in their own assets [Fama and French, 1996; Chua et al., 2007; Malighetti et al., 2011]

Formulation of research hypotheses

As a dependent variable report examines Price-To-Book Value Ratio.

The first model factor is the company's return on assets (ROA, Return On Investment), which is calculated as the ratio of net profit and the total of its assets. High return on assets of the company is its competitive advantage and, therefore, an indirect factor influencing on the creation of shareholder value [Olsen et al., 2006] Thus, the first research hypothesis is formulated as follows:

H1: The higher the return on assets of the company, the greater its investment potential.

Another factor model is financial leverage, or the proportion of long-term debt in the financing structure of the company (DR, Debt Ratio). Past empirical studies presented financial leverage as a tool, disciplining company's management and reducing agency costs. Thus, a high proportion of long-term debt is able to have a positive impact on the creation of shareholder value

H2: The higher the proportion of long-term debt of the company, the higher the investment attractiveness of the company.

Creating a company's shareholder value is directly related to the investment decisions made by management Empirical studies show a direct dependence of the level of investment activity and investment potential of the company. Investment activity coefficient can be defined as the ratio of non-current assets in the form of long-term investments, investments in tangible assets and construction in progress to the total value of non-current assets. Thus, the third research hypothesis is formed as follows:

H3: The higher the investment activity of the company, the higher is its investment potential.

Following exogenous variable model is the size of the company, as the shares for large diversified companies, which are more likely to have stable cash flows in the future, investors are willing to pay a "premium." There are two ways to calculate the proxy variables that show the size of the company: as the logarithm of the company's revenues or as the logarithm of the total assets of the firm. In the empirical study of GSOM professors it is indicated that logarithm of revenue is relevant to measure the size of companies with a high proportion of intangible assets [IV Berezinets, AV Razmochaev, DL Volkov, 2010]. Russian electric power sector companies are characterized by very low proportion of intangible assets. In this regard, it is better to use the natural logarithm of the total assets of the company, which, according to Fama and K. Yu French [Fama, French, 2002], takes into account company's risks.

H4: The larger the company is, the higher its shareholder value.

The final factor included in the model, is the age of the company, which, according to many empirical studies, has negative impact on the investment potential of a company that can easily be explained by the life cycle theory [Malighetti et al., 2011].

H5: The longer a company operates, the lower its investment potential.

The companies in sample and description of variables

Within this empirical study examined Russian companies belonging to the electricity industry. Companies in the sample selection criteria are as follows: First, in order to be able to analyze the multiplier price / book value, the factor of tradability of all companies in the sample on the Russian Trading Stock Exchange is indispensable. Further, sample values have to reflect the process of creating shareholder value, that is why the selection parameter is set - the net profit. Thus, in the sample present the largest representatives of the industry with net profit of more than 1 billion rubles. And the last important selection parameter is the main activity of the company: to conduct research properly it is necessary that the principal activity of the company is directly connected with the production or transmission of electricity.

In the study a sample of data on 39 public Russian companies in 2012 is used. Period is chosen based on the fact that the data in 2012 is relevant and sufficiently reflect the current situation in the industry. On the other hand, using this period it is possible to get the most comprehensive data pool, as many data for 2013 in the Company's public reports are not available yet. Enterprises reporting database “SCREEN” serves the source of financial information about the selected companies.

Since all companies of the sample operate on the territory of Russian Federation, it is assumed that such uncontrollable environmental factors as economic and political situation in the country, the national currency, the level of competition in the industry, the legal framework governing the conditions of the companies are the same for all representatives of the sample.

Thus, the sample includes the measures required for the calculation of relative indicators that will be used as factors in the regression:

- Total non-current assets

- Total current assets

- Equity

- Current liabilities

- Long-term liabilities

- Revenue

- Net profit (loss)

- Construction in progress

- Income-bearing investments in tangible assets

- Financial Investments

Quantitative research variables:

- mbvalue = Market Value / Book Value

- roa = NI / TA - return on assets

- dr = Long-Term Debt / Total Debt - the proportion of long-term debt in the financing of the company

- invact – share of investments in tangible assets, financial investments and construction in progress in the general non-current assets

- size = ln (TA) - the size of the company as the logarithm of total assets

- age - age of the company, years

The Empirical Study

In the study an existing model is used to check the results for data on the companies belonging to the electricity industry.

Summary statistics:

Table 1 – Summary statistics

| Variable | Number of observations | Mean | Standard deviation | Min | Max |

| mbvalue | 39 | 0.7774 | 0.5703 | 0.0763 | 2.1221 |

| roa | 39 | 0.1334 | 0.1043 | 0.0094 | 0.3749 |

| dr | 39 | 0.1967 | 0.1576 | 0 | 0.5649 |

| invact | 39 | 0.1650 | 0.2307 | 0 | 0.9999 |

| size | 39 | 24.2948 | 1.4024 | 21.1508 | 27.7588 |

| age | 39 | 9.2820 | 1.9049 | 6 | 14 |

Average value of Tobin's coefficient for companies in the sample is 0.7774, but the largest standard deviation can determine that the range of values is very large. There are companies with Price-to-Book Value Ratio less than 0.1, but also present companies with very high coefficient values - more than 2.

Return on assets of electric power companies is on average 13%, and the range of values is also quite large. As for the proportion of long-term debt, there are companies that do not use long-term sources of funding, and the maximum value of the index in the sample is 56.5%.

Investment activity coefficient, showing the ratio of financial and profitable investments in tangible assets to the total value of non-current assets, is, on average, 16.5%, but the range of values is also very large.

As for the size of the company, for this indicator there is a slight standard deviation as the sample of companies is carried out by "net profit of not less than 1 billion rubles," and objects are relatively homogeneous. Age of the company is ranged from 6 to 14 years.

The model verification

As in the baseline study, we consider a linear model where the dependent variable acts Price-To-Book Value coefficient, and factors - return on assets, the share of debt in the financing of the company, the ratio of investment activity, the size and age of the company.

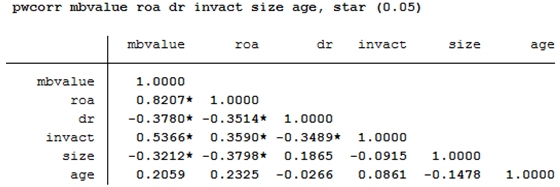

First, the correlation matrix was constructed in which asterisks denote significant correlation coefficients (significance level 0.05). So we see that the correlation coefficients are significant variable mbvalue with all the factors except age of the company. [See Appendix 5]

According to the results we can reveal the strength and direction of the relationship between the variables:

- ρ (mbvalue; roa) = 0.8207; - A strong positive correlation

- ρ (mbvalue and dr) = - 0.3780; - Average negative correlation

- ρ (mbvalue and invact) = 0.5366; - Average positive correlation

- ρ (mbvalue and size) = - 0.3212; - Average negative correlation

- ρ (mbvalue and age) = 0.2059; - A weak positive correlation

Fig. 1 – Correlation matrix

We estimate the parameters of the model of the form:

Y = MBValue = β0+ β1*roa + β2*dr + β3*invact + β4*ln(TA) + β5*age + ɛ

Using the statistical package Stata, we obtain estimates of the coefficients of the regression model, so it takes the form:

Y = 0,3546+ 3,8284*roa – 0,1203*dr + 0,6683*invact - 0,0089*ln(TA) + 0,0047*age

Statistical significance of the model can be tested using the Fisher exact test, which is based on Fisher statistics having a distribution with m1 = (m-1), m2 = (n-m) degrees of freedom (significance level 0.05). So, in our case m1 = 6-1 = 5, m2 = 39-6 = 33, right-critical region, we check the hypothesis of the form:

H0: β0=0, β1=0, β2=0, β3=0, β4=0, β5=0;

Ha: β02+ β12+ β22+ β32+ β42+ β52≠0;

Regression model is significant, as P-Value = 0.00<0.05, and we can accept the alternative hypothesis Ha. The determination coefficient R2 = 0.7424, which indicates reasonably good explanatory power of the model.

Evaluation of the factors significance

Then we test the significance of regression model factors to test the hypothesis:

Н0: βj=0, j= 1, m-1

На: βj≠0.

We check the importance of the factors using the statistics with the Student distribution, (n-m) degrees of freedom at a significance level of 0.05. Thus, (n-m) = 33, two-sided. We check the importance of the factors, using Stata package and P-Value of each coefficient.

Several model factors, as well as constant proved to be insignificant:

- β1: P-Value = 0.000<0.05 → Ha accepted, coefficient is significant, indicating the significance of the factor - return on assets, roa;

- β2: P-Value = 0.737>0.05 → H0 accepted, coefficient is insignificant, suggesting an insignificant factor - financial leverage, dr;

- β3: P-Value = 0.009<0.05 → Ha accepted, coefficient is significant, indicating the significance of the factor - investment activity coefficient, invact;

- β4: P-Value = 0.820>0.05 → H0 accepted, coefficient is insignificant, suggesting an insignificant factor - the size of the company, size;

- β5: P-Value = 0.865> 0.05 → H0 accepted, coefficient is insignificant, suggesting an insignificant factor - the age of a company, age;

- β0: P-Value = 0.730> 0.05 → H0 accepted, constant is insignificant

Eventually, we obtain two significant factors in the model on which to draw conclusions:

➢ β1 = 3,8284 - positive coefficient of the variable roa, consequently, by increasing the profitability of the company's assets per unit, P / book value increases by 3.83 on average. Or by increasing the return on assets of 1% Price-to-Book Value Ratio is increased by 3.83%.

➢ β3 = 0,6683 - positive coefficient of the variable invact, consequently, with an increase of investment activity coefficient by 10%, the price / book value increases by an average of 6.68%.

Since the remaining coefficients of the model are insignificant, we can not draw conclusions about their impact on the dependent variable.

Model quality assurance

Under the conditions of the Gauss-Markov, linear regression functions parameter estimations have the properties of unbiasedness, consistency and efficiency. Thus, the variance of the random component of the model is constant ɛi: V [ɛi] = σ2. If this condition is violated, parameter estimations lose the property of consistency and efficiency, which affects the results of the analysis of the significance of the model and its parameters. Therefore we carry out Breusch-Pagan test to check whether there is heteroscedasticity in the model.

With the implementation command estat hettest in Stata we obtain a probability of Prob = 0.0001 <0.05, so we accept the null hypothesis H0, which means that the variances errors are equal and the problem of heteroscedasticity is absent in the model.

Since we have got significant regression model with high coefficient of determination R2 = 0.7424, but three factors and constant are insignificant and the standard errors of regression coefficients are high, it is necessary to test for the presence of multicollinearity.

To do this, when implemented in Stata command regress, we use the VIF (Variance Inflation Factor). Since the resulting values of VIF do not exceed 4 for each of the factors, we conclude the absence of multicollinearity in the model.

Testing of research hypotheses

The first hypothesis H1 is accepted: «The higher the return on assets of the company, the higher its investment potential", as the first factor is significant and positive, so dependence is directly proportional.

The second model factor is proved insignificant, so we can neither accept nor reject the second hypothesis of the study: H2 «The higher the proportion of long-term debt of the company, the higher the investment attractiveness of the company."

The third hypothesis H3 is accepted: «The higher the investment activity of the company, the higher its investment potential" as the third factor is significant and positive, so dependence is directly proportional.

The fourth model factor is proved insignificant, so we can neither accept nor reject the fourth hypothesis of the study: H4 «The bigger the company is, the higher its shareholder value."

The fifth model factor is proved insignificant, so we can neither accept nor reject the fifth hypothesis of the study: H5 «The longer a company operates, the lower its investment potential."

Finally, the empirical study has shown the positive correlation of Price-To-Book Value of a company and its ROA and investment activity coefficients. That is why Russian electricity sector companies need to increase return on assets and investment activity become more attractive for investors.

References

- Березинец И. В. Основы эконометрики. Учебное пособие / И. В. Березинец; Высшая школа менеджмента СПбГУ. – 4-е изд., испр. и доп. – СПб.: Изд-во «Высшая школа менеджмента», 2011.

- Детерминанты создания акционерной стоимости российскими компаниями / Анкудинов А.Б., Лебедев О.В. / Электронный журнал «Корпоративные финансы», №1(29). – 2014.

- Valuation of Internet Stocks – an IPO Perspective. / Bartov E., Mohanram P., Seethamraju C. / Journal of Accounting Research, no. 40, pp. 321–346. - 2002.

- Variance Bounds Tests and Stock Price Valuation Models. Journal of Political Economy - vol. 94. no. 5/ Kleidon A. - 1986.

- What Drives Shareholder Value. Asian Academy of Management Journal of Accounting and Finance, no. 1 / Pandey I. - 2005.

- How Do Accounting Variables Explain Stock Price Movement.Theory and Evidence. Journal of Accounting and Economics, no. 43 / Chen P., Zhang G. p. 219. - 2007.

- Ownership Structure and Value of the Largest European Firms: the Importance of Owner Identity. Journal of Management and Governance, no. 7 / Pedersen T., Thomsen S., p. 27. - 2003.

- Multifactor Explanations of Asset Pricing Anomalies. Journal of Finance, vol. 51 / Fama E., French K., no. 1. - 1996.

- Value Determinants in the Aviation Industry. Transportation Research Part E: Logistics and Transportation Review, vol. 47 / Malighetti P., Meoli M., Paleari S., Redondi R., no. 3 - 2011.

- Финансовые решения российских компаний: результаты эмпирического анализа / И.В Березинец, А.В. Размочаев, Д.В. Волков / Вестник Санкт-Петербургского Унивеситета. – 2010 [Электронный ресурс] // Сайт vestnikmanagement.spbu.ru. – Режим доступа: http://www.vestnikmanagement.spbu.ru/archive/pdf/453.pdf, свободный. – Загл. с экрана.

- Оценка эффективности управленческих решений [Электронный ресурс] // Сайт books.ifmo. – Режим доступа: http://books.ifmo.ru/file/pdf/818.pdf, свободный. – Загл. с экрана.

- Показатели эффективности организации [Электронный ресурс] // Сайт psylist.net. – Режим доступа: http://psylist.net/socpsy/00019.htm, свободный. – Загл. с экрана.

- Экономика предприятия: понятие и виды эффективности [Электронный ресурс] // Сайт aup.ru. – Режим доступа: http://www.aup.ru/books/m203/9_5.htm, свободный. – Загл. с экрана.

- KPI (Key Performance Indicators): разработка и применение показателей бизнес-процесса. Показатели эффективности / Business Studio [Электронный ресурс] – Режим доступа: http://ru/procedures/business/kpi/, свободный. – Загл. с экрана.

- Ключевые показатели эффективности [Электронный ресурс] // Сайт ru. – Режим доступа: http://www.elitarium.ru/2011/04/01/kljuchevye_pokazateli_jeffektivnosti.html, свободный. – Загл. с экрана.