DEVELOPMENT TREND OF MANAGEMENT ACCOUNTING AND USAGE

Сарантуяа Б.

Доктор, Управление бизнес-индустрии, Монгольского Государственного Университета Науки и Технологии

ТЕНДЕНЦИИ РАЗВИТИЯ УПРАВЛЕНЧЕСКОГО УЧЕТА И ИСПОЛЬЗОВАНИЯ

Аннотация

Эволюция уроки управления и бизнес-истории стоить и управленческого учета информация делится на 4 этапа развития.

Ключевые слова: стоимость расходов, финансирование и бюджетирование.

Sarantuya B.

Ph.D, Department of Business Administration of Mongolian University of Science and Technology

DEVELOPMENT TREND OF MANAGEMENT ACCOUNTING AND USAGE

Abstract

Evolution of management and business history lessons cost and management accounting information is divided into 4 stages of development.

Keywords: cost, Zero based budgeting, methods.

Globalization, history lesson, part of the process of restructuring and management reform and perfect information network and product and service quality, cost savings become a significant focus on Southeast Asia, China, America, Japan, Germany, materials handling, near the capital expenditure. They regional economic globalization, and began to head competition. All of this on a log management is a significant link between the introduction of the production methods.

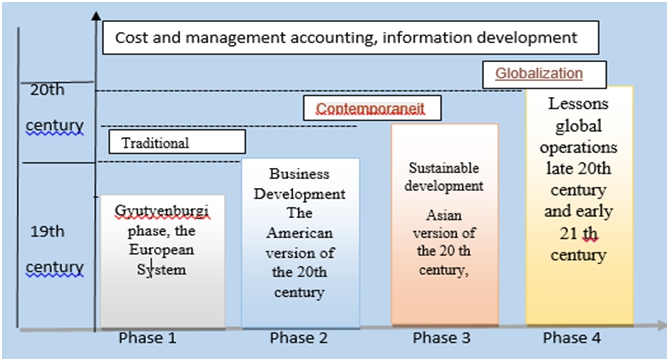

Evolution of management and business history lessons cost and management accounting information is divided into 4 stages of development.

Figure 1.1 - Stage of development of information management.

Table 1 - Management accounting and development

| Frequency | The feature |

| Phase 1. Iosial Vyejvüüd, Johannes Gyutyenbyergi phase of the European System of the XIX century | · Cost data analysis included changes in consumer prices · Initiated cost accounting · Estimated makeup for each material and labor costs · Described absorbent costs · Defined value measurement principles · FIFO method was used · Price only the set of direct materials, direct labor, considered part of the cost. · Industrial action was to analyze a problem only when costs exceed |

| Phase 2. Business DevelopmentThe American version of the 20th century | · Defined strategic planning · Defined management system · A monthly report to be created · Developed a flexible budget · Defined standard costs · Reported Responsibility Report · Created fluctuation analysis · Described the decentralized control system · Vouchers defined control system · The cost of traditional systems transferred to the classical typology · Business risk could be perfect for budget deficits · Does not reflect the full economic benefits |

| 3. Sustainable development Asian version of the 20 th century, | · Implemented a foundation for quality control · User group for increased participation · Evaluation system has been established · Automated transformation · Testing, design and quality parameters are defined in a cycle of conversion · Described national strategy · Copied directly from the experience in some countries |

| 4. Lessons global operations late 20th century and early 21 th century | · Structural changes in the way described · Emphasizes the evolution of management · Information network specific · Conditions, reducing the cost of increased · Just-in-time system created · The cost of direct labor system established relationship · High-quality, low-price policy developed · Failed to take account of local and regional features complete · Decrease in the value of information likely to increase |

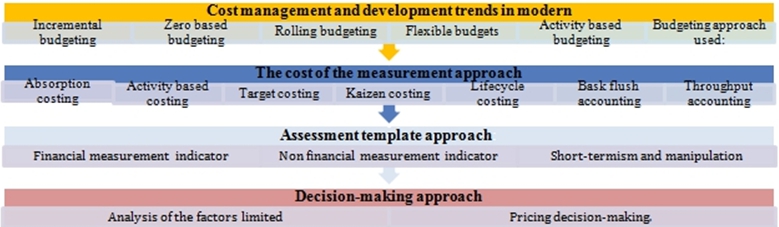

Figure 1.2 - Сost management and modern development trends

Organization and the task of the main reasons for the success of its internal data and the management team of the organization is to provide the necessary information to make sound management decisions. Enterprises and accounting operations, the following common issues are unresolved. Including:

- Lack of management accounting, cost accounts contain important information

- Dominant focus on financial accounting and management record keeping and analysis methods used in practice are not primarily.

- Management accounting, higher education is investigating the theoretical framework.

- Business organization's management team to provide the necessary information to make sound management decisions are at the early stages of almost missing.

Our state has implemented a good financial records, but the record has not been fully implemented. Management accounts recorded a rapid decision-making object inventory management analysis, design and create a comprehensive system to monitor. For example:

- Increase in labor productivity

- Support management decision-making

- Support management decision-making, decision making, and managing the organization and to ensure optimal to organize

- Implementation of the organization's strategic objectives and control activities and improve risk detection and prevention opportunities

- Market competition and increasing opportunities to improve resolution

- Introduction of new technologies, and provide the opportunity to keep up with the social development

- Together with the trust in management and goal of creating intimate atmosphere for everyone to support the retention effort

- Improve the culture of the organization and improve working conditions

- Organization's reputation grew, elevated position in the market

- Improve the management responsibilities

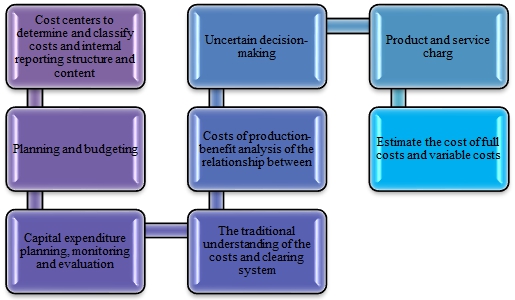

Management accounting is the most important element in the form of a requirement for integrated data preparation. Therefore, companies and organizations in the management accounts use 8 to 14 using the method of analysis. Including:

Figure 1.3 - Management decision-making methods In implementing this method, it is important to use the following methods.

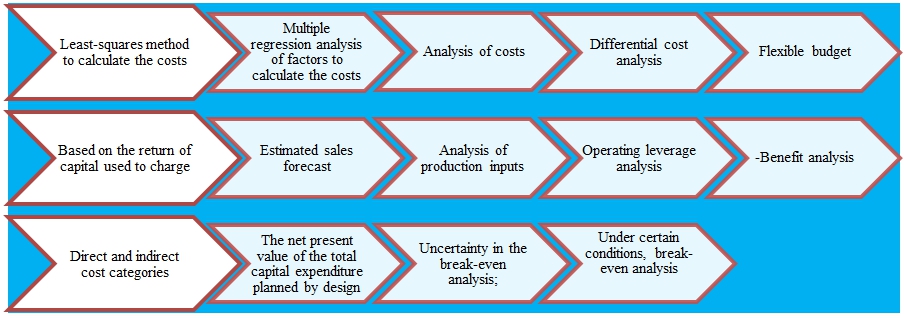

Figure 1.4 - Applications management accounting methods

References

- Agvaan N, Erdenesuvd.L”Analysis of Finance and Economy” UB .1997

- Bayrma ”Management accouting ” UB. 2000

- T “To change the management accounting system problems” UB.2003