БИЗНЕС И УПРАВЛЕНИЕ

Сарантуа Б.

Доктор Профессорная команде экономика и финансого, Института Комьпютерном Техника и Менежмента, Монголского Государственного Университета Науки и Технологий

БИЗНЕС И УПРАВЛЕНИЕ

Аннотация

С 1990 года в странах и регионах возникли благоприятные обстоятельства по глобализации бухгалтерского учета, таким образом, его данные шаблоны стали одинаковыми. В рамках процесса глобализации и его истории, многие страны стали уделять существенное внимание структурным реформам экономики, менеджменту данных и информации, качеству продуктов и услуг, включая эффективность затраты.

Ключевые слова: Стоимость расходов, Информация данных, Финансирование и бюджетирование.

Sarantuya.B

2PhD in business administration,Economics and Finance professor’s team, Technological School of Mongolian University of Science and Technology

MANAGERIAL ACCOUNTING, ITS INTERNATIONAL CONCEPTS AND DEVELOPMENT TENDENCY

Abstract

Since 1990 in countries and regions favorable circumstances have emerged on globalization of accounting thus its data templates have become identical. In the framework of the globalization process and its history, many countries started to pay significant attention to structural reform of economy, management renovation data and information perfect network, quality of products and services including cost efficiency. One big example of these has been Southeast Asia and China’ s economy has grown, the regional labor and material processing has grown and capital assets consumption reached to USA and Japan level. Hence, they started leading the economy and globalization competition. These have been explained with management registration methods were it has been introduced in industry and services. In this article aimed to define management development tendency, it’s importance based on the summary research of foreign researchers’ managerial accounting comparative study.

Keywords: Cost Expenditure, Information Data, Financing and Budgeting.

Current economy’s fast information technology development, social development speed enables economy freedom for producers and final responsibility of operation increases day to day, date information required for making management decision which takes final responsibility. This information needs and its flow being provided by accounting structure, approximately almost 80-85% of the information and data being produced by industry and enterprises are being provided through accounting registration system. Therefore, the accounting registration system is being considered as a “business language”

Accounting is a management tool with its own methodologies for efficient governance of assets and properties in businesses and economic entities with various fields. There are three different types of possession (joint owned cooperative, companies) one of them is private, state and joint venture possessions. When carrying out research and managing the aforementioned possession types, accounting has played significant role. In order to develop the accounting many scholars and researches made number of studies. Herewith, I’m presenting 14 study works of 20 scholars.

Herein:

- Thomas Ahrens, professor Barvick Business University, Christopher S Chapman, Head of the Accounting Registration Department , Seid Business University in their work “New measures in performance management” they have defined that the possibility of replying BSC (balanced scorecard) tools on mutual coherence of money indicators and management registration, and shareholders, whether the data base could be integrated as a whole, the economic entities could reflected in a balance thoroughly, whether it could meet the contemporary development tendency, is there any funding asset sources for shareholders for business union possibility and its influence for individuals, whether can carry out monitoring for shareholders etc.

- Stanley Baiman, professor, Pennsylvania University and PhD in Accounting, Stanford and Guide University in his study ”Contract theory analysis of managerial accounting issues” has summarized the certain reason and disputes of production and tried to define the preliminary hypothesis on compensation agreement planning .

- Jane Baxter, professor of Sidney University, and Wai Fong Chua, professor of Accounting Sheffield University and Sidney University, Consultant and representative of Financial Committee and UNSW in their study “Reframing management accounting practice: a diversity of perspectives” they studied multilateral general conception and approaches of management accounting practice and its reframing. They summarized future changes and its integration with management activity. They referred to goal of management and services, as well as institutional strategy with its optimal way, with its economical and efficient output sales increase

- Alnoor Bhimani , critic of Finance and Accounting , London University, PhD in Management accounting of University of Canada and Cornel University referred to his work ”Management accounting and digitization” that price management tendency, activity based management economy coherence, LEC, price management purpose, profit income analysis for customers, strategic investment cost value/ estimation. He defined the concept as administrative process would depend on the technological investment ratio. In result, he proposed to move the management accounting into digitization”

- Robert H. Chenhallm professor of Finance and Accounting Monash University, professor of James Cook University. In his work “The contingent design of performance measures” proposed to use combined performance and non financial, as economical measures as the latest changes to improve institutional operation

- Robin Cooper, management accounting professor of Goyzueta Business University ,Regine Slagmulder accounting professor of Tilburg University, Netherlands, professor of accounting and monitoring of INSEAD made study ”Integrated cost management”. In their work, first of all, they expressed that management accounting should be modules. They also carried out their study on the Olympus, Komatsu, Isuzu, Tokyo Motors corporations’ activities and divided cost accounting program into internal and external.

- Lawrence A. Gordon, PhD and director of Lawrence, Gordon Н. Smith Business University, professor of Management accounting, and Insurance Data. He has been giving lectures in universities of Harvard, Columbia, Toronto, London, Mellon, Martin P. Loeb member of Gordon Н. Smith Business University, Insurance Data and accounting professor, professor of North America University, Chih-Yang Tseng, professor of Н. Smith Business University and Manila and Business University. In their work “Capital budgeting and informational impediments: a management accounting perspective” data information and zonal development issues will burden in management accounting perspectives. They also referred to as one of the most crucial issues is preparing capital planning. They proposed to use price management capital assets in capital planning.

- Keith Hoskin,professor of accounting and strategy of Barvick University, Richard Macke professor of accounting of Finance and Economical University of London, John Stone, senior lecturer, London King College, and Dean of History, Valencia University wrote in ”Accounting and strategy: towards understanding the historical genesis of modern business and military strategy” that accounting and business strategy have always been associated with the agreements and actual consumption. Therefore summarizing the contracts which have been proven by the management strategy practice prevents from business risks as well as they have defined that this will play as an entry passageway to equal development within short term.

- Lisa Kurunmaki, lecturer and PhD in accounting, London University of Economics, Peter Millet, professor of management accounting, London University of Economics and Finance, members of Coordination and Piloting Centre reflected in their ”Modernizing government: the calculating self, hybridization and performance measurement” work about main institutional governance conception, institutional reform, efficient governance module, best practices of institutional governance and their main assumption. They also defined modern governance performance indication come into control view.

- Eva Labro, lecturer of London University of Management Accounting, PhD of Leuven University in his work ”Analytics of costing system design” proposed to use costing analytics in managerial accounting on decision making.

- Kim Langfield-Smith, PhD in Management accounting, professor, Finance and Accounting Department of Monish University of Australia, in his work ”Understanding management control systems and strategy” aimed to give an understanding for public, explanation by research of correlation between management control systems and strategy, loan allocation compliance with the contracts and its use and importance. He also defined implementation basis of understanding management control systems and strategy is one of the main issue of institution’s structure. Thus, he proposed modules of МCS /management control systems/, BCS /budgeting and control systems/

- Allan Hansen ”Management accounting, operations and network relations: debating the lateral dimension” Allan Hansen assistant professor, Kopegan University of Business, in his ”Management accounting, operations and network relations: debating the lateral dimension and its lateral dimension ” defined the importance of managerial accounting, operations and its network relations in the following three directions. Such as;

- Research outcomes showed that management accounting has showed the consequence differences.

- To some extent management accounting exists in industrial environment.

- Accounting estimation creates management activity room for managing non financial, one- lined data. He also defined external reform of internal control’s significance directs to internal matters.

- Hanno Roberts, professor of management accounting and control, Management University, Oslo. In his work ”Management accounting intelligible” considered multilateral perspectives of keeping managerial accounting track focuses on creating the best practices of the two different world. The issue of management, functioning implementation, what followed principles are influential to managerial accounting in terms of institution’s technical aspect and innovations. Furthermore, he considered the management functions and principles as follows:Management functioning: 1. Planning, 2. Erecting, 3. Coordination, 4. Directing. Management principles: 1. Work Units, 2. Administration, 3.Discipline, 4. Unity of Resolution, 5. Direction Unity, 6. Industrial management interest should match with the overall interest, 7. Payment, 8. Centralization 9. Chain Continuity, 10. Regulation, 11. Loyalty, 12. Individual Stability, 13. Initiation, 14.Solidarity

- Kazbi Soonawalla,PhD in Business Management, Stanford University who carries out finance reporting and research on international accounting. He brought a change in managerial accounting development with his work called ’Environmental management accounting”. As a result, he regarded that in order to develop strategic policy on environmental managerial accounting to reflect further cost change and its compliance He also defined that its indicators should be used in decision making level

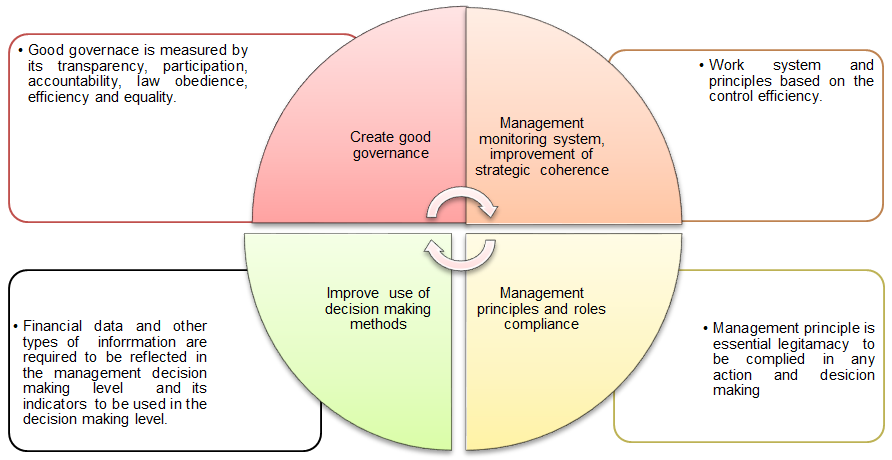

Aforementioned scholars’ research revealed four directions of managerial accounting.

Chart 1 - Conception Directions

Concepts on management accounting which were developed and defined by scholars have been defined as institutional joint management or good governance, management principles, management control system, well developed true data and information, the way of using them in the decision making or institutional management, close connection with its strategy and management accounting tendency. In other words, in order to improve institutional planning on short, medium and long terms, management, arrangement and its outcome and efficiency, management accounting based on the accounting well developed database is crucial and demanding in terms of theory and practice.

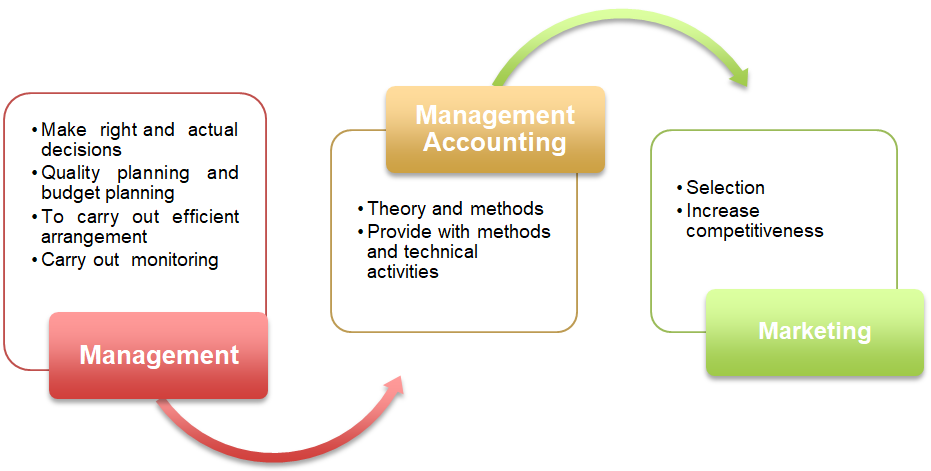

Map 2 - Development Tendency

Importance of institution’s managerial accounting has been in the following three parts. Such as:

- To implement an aim to work efficiently and economically

- To carry out analysis on whether certain industry and services work with outputs and summarize the data

- To give an answer whether has achieved the aim.

For the managerial level staffs that are in charge of industry and services of a certain economic entity, the main responsibility should be focused on accounting, estimation, planning, budgeting and research. ” Managerial Accounting” is one of the main accounting responsibilities of financial managers, accountants which have to be carried out in the market economy

A managerial level staff without managerial accounting cannot obtain perception of cost expenditure of a unit product production and unit service as well as outcome performance data and information. Therefore every managerial staff and accountant should have a certain understanding of managerial accounting to some extent and it is crucial for them and to keep managerial accounting record in his or her work. The two types of the financial and accounting may sound different but their final goal is amalgamated. Thus their specific of difference is the financial accounting and it covers all activity of the economic entity and provides all financial and economical data & information in terms of assets and resources. Managerial accounting focuses on the internal matters and plays significant role in making optimal decision in order to make the products and services efficient, low cost and good quality.

Depending how well and true managerial accounting record is being kept the economic entity’s participation in the market relations and business activity prospect and vision can be foreseen and estimated well.

In result, the of assets utilization improvement possibilities can be estimated and defined the income earning current value correctly and reach to an understanding of revenue increase by this can foresee its implementation possibilities. This will bring the economic entity into success.

Also, accounting is a coherent understanding which covers all internal aspects of an economic entity. It contains the core of internal accounting system as cost expenditure and results estimation coherence. Its final end is, to define certain organization’s policy, strategy and guidance.

In order words, managerial accounting has its main purpose and significance in carrying out research on future cost expenditure during productivity and services of a certain economic entity, its structure, the reason of decrease and increase, correlation of final possibilities and cause and develop policy and strategy, its compliance.

Developed countries in market economy, the managerial accounting record has been kept in the aforementioned purposes and implemented with its actual quality. Furthermore, it is impossible to consider the managerial accounting as identical to planning, budgeting, data and research including control system of centralized planned economy.

Список литературы

Agvaan.N , Erdenesuvd.L "Analysis of Finance and Economy " UB , 1997

Моломжамц, "Удирдлагын бүртгэл", УБ, 1999

Б.Баярмаа, "Удирдлагын бүртгэл", УБ, 2000

С.Жамъяансүрэн, "Бизнесийн шинжилгээ", УБ, 2000 он

Н.Агваан, "Аудит", УБ, 2001 он

С.Өлзийбат, "Удирдлагын бүртгэл", УБ, 2002 он

Н.Агваан, Л. Эрдэнэсувд, П. Баянсан, Т. Лагнай нар "Удирдлагын бүртгэл", УБ, 2005

Н.Агваан, "Нягтлан бодох бүртгэл", УБ, 2008 он

Charles T.Horngren, Gary L.Sundem "Introduction to Management accounting", 8-th edition, USA

Ronald W.Hilton " Managerial Accounting", 3-d edition, USA

Ray H.Garrison, Eric W.Noreen " Managerial Accounting", 8-th edition,

Chase Aquilano Jacobs "Production and Operation Management