УПРАВЛЕНИЕ ЭФФЕКТИВНОСТЬЮ КАК ФАКТОР ПОВЫШЕНИЯ КОНКУРЕНТНОСПОСОБНОСТИ

Стасевич Д.И. 1, Калугина А.Д. 2

Кандидат экономических наук, доцент, РЭУ имени Г.В. Плеханова 1 , Аспирант, РЭУ имени Г.В. Плеханова 2

УПРАВЛЕНИЕ ЭФФЕКТИВНОСТЬЮ КАК ФАКТОР ПОВЫШЕНИЯ КОНКУРЕНТНОСПОСОБНОСТИ

Аннотация

В статье рассмотрены основные аспекты повышения уровня конкурентоспособности в организациях на базе системы сбалансированных показателей. Предложены механизмы оптимизации в процессно-ориентированных стратегического и операционного управления в организациях на базе концепции управления эффективностью.

Ключевые слова: Стратегический менеджмент; Стратегия; Система сбалансированных показателей; ССП, Управления эффективностью; Бизнес-процесс, Конкурентоспособность.

Stasevich D.I.1, Kalugina A.D.2

PhD, Senior Lecturer, Plekhanov Russian University of Economics1, Postgraduate student Plekhanov Russian University of Economics2

PERFORMANCE MANAGMENT AS A FACTOR OF INCREASED COMPETITIVENESS

Abstract

This article is devoted to corporate performance management in organizations. The article describes the main aspects of improving the competitiveness of a company in process oriented organization on the basis of the Balanced Scorecard system. Author suggests the mechanism of optimization of the strategic and operational management in the process-oriented organization based on the concept of corporate performance management.

Keywords: Strategic Management; Balanced Scorecard; Business Process Management; Business Performance Management; Performance measurement; CPM; Strategy.

Nowadays in order to achieve the dominate position on the market, companies have to take into account both financial and non-financial factors of competition, because of highly vigorous competition. On the one hand, organizations have to ensure sustainable growth of company`s performance and operation`s efficiency, on the other hand – effectiveness of strategic goals execution for maintaining the required level of competitiveness and overall strategic development of the organization.

The process of strategy implementation is carried out together with operating activities, in which the main objective is performing initiatives for indicators. The core objective business performance is a balance between strategic development and economic efficiency in the current term. Moreover, the combination of these objectives and coordinated management is essential in strategic change management. In other words, both control system, that provide ongoing performance indicators of the company, and the process control system implementation in the organization have to be presented in organization.

At the present time a lot of methodologies and performance management tools have already developed even taking into account attunement that provides strategic and operational improvement. Users of these systems are different management role group: owners and managers, a group of top management and a group of mid-level management.

Well known models of strict logical linking of standard financial indicators. A good example is a DuPont model (also known as the DuPont identity or the DuPont method). Effective business management model is used for the performance attribution of average weighted cost of capital. Usually the DuPont method is understood as the algorithm of the financial analysis of return on assets of company, where profit margin is multiplied by asset turnover and equity multiplier. The methodology reflects three important components: the structure of business risks; the dynamic of risk, and additional cost of capital.

As noted above, the constantly increasing level of competition that makes it necessary to use non-financial indicators of performance in the governance. As a result there is a growth in share of the business performance systems of governance, allowing taking into account both financial and non-financial performance. In the last decade, the Balanced Scorecard (BSC) is one of the most widely used strategic management tool.

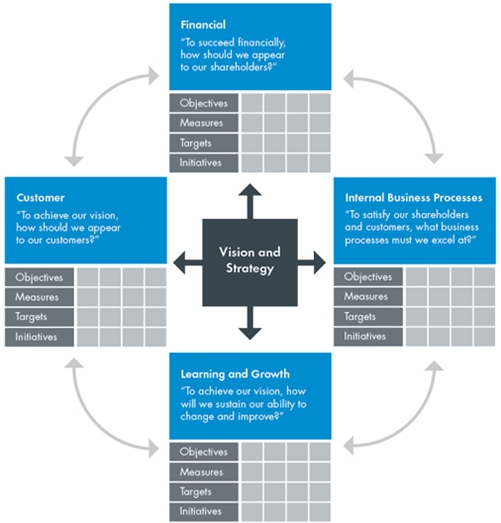

The Balanced Scorecard concept, popularized by Robert S. Kaplan and David P. Norton, is a performance management tool that encompasses the financial measures of an organization and key non-financial measures relating to customers or clients, internal processes, and organizational learning and growth needs (see Figure 1). It places these into a concise “scorecard” that can be used to monitor performance. The Balanced Scorecard process attempts to identify important links between financial performance and the underlying customer, internal processes and organizational metrics. This creates a mechanism for translating the strategic vision into concrete actions necessary to achieve success [3,17].

Fig. 1 – Balanced Scorecard framework [ 3,18]

In terms of aggressive competition BSC enables organizations to respond quickly to changes in the external environment through the use of clear performance indicators of each employee and their possible adjustment for the operational management level. Four basic “perspectives” allow companies to focus on priorities in the development and ensure their attunement.

A separate element the performance management system can be called the application in the organization of the process approach to management.

A business process is a collection of related, structured activities or tasks that produce a specific service or product (serve a particular goal) for a particular customer or customers. There are three main types of business processes [2,35]:

- Management processes that govern the operation of a system. Typical management processes include corporate governance and strategic management.

- Operational processes that constitute the core business and create the primary value stream. Typical operational processes are purchasing, manufacturing, marketing, and sales.

- Supporting processes, that support the core processes. Examples include accounting, recruitment, and technical support.

The combination of business process approach and Balances Scorecard system provides additional synergy in terms of quality performance management. This effect discovers the possibility of monitoring the effectiveness of all key business processes in the organization by incorporating appropriate objectives on their optimization in the projection of the "internal business processes” Balanced Scorecard. Such a mechanism provides a sufficient strategy to focus on operational efficiency, as well as provide the necessary balance between the strategic and operational objectives through expert analysis of cause-and-effect relations between objectives increase the efficiency of business processes and strategic objectives.

The process of identifying cause-and-effect relations between the perspectives of “Internal Business Processes” and “Clients” to determine what kind of business processes is essential that leads to the identification of clear priorities in the implementation of these optimization problems, or business process reengineering. As part of the subsequent process of cascading every employee involved in the appropriate process within the strategic map of BSC formalized unique objectives directly related to its activity, thereby providing broadcast by BSC main objective of optimizing operational management on the low level. We should also highlight that the employee in this case can be achieved, as related to the strategy objectives expressed in the performance of the business process in which it is involved, and the tasks related to the efficiency of the process.

References

- Стасевич Д.И. Стратегическое управление компанией на основе сбалансированной системы показателей (на примере финансовой организации): Дис. канд. эконом. наук. М., 2012.-17-20.

- Стасевич Д.И., Ляндау Ю.В. Теория процессного управления. // М.: Изд-во ИНФРА-М., 2012.35-36.

- Каплан Роберт С., Нортон Дейвид П. Организация, ориентированная на стратегию. // М.: ЗАО «Олимп-Бизнес», 2004.17-20.

- Маркова В. Д., Кузнецова С. А. Стратегический менеджмент. // М.: Инфра-М; Новосибирск: Сибирское соглашение, 2007.

- Хаммер М., Чампи Дж. Реинжиниринг корпорации: Манифест революции в бизнесе. // СПб: Изд-во Санкт-Петербургского университета, 1997.

- Porter M., Competitive Advantages // Free Press, NY, 1985.