ВЛИЯНИЕ ИНФЛЯЦИИ НА АНАЛИЗ ОСНОВНЫХ ФОНДОВ

Калуби Р.Д.М.

ORCID: 0000-0003-4016-0861, Аспирант 3-го года обучения, Санкт-Петербургский Государственный Политехнический Университет Петра Великого

ВЛИЯНИЕ ИНФЛЯЦИИ НА АНАЛИЗ ОСНОВНЫХ ФОНДОВ

Аннотация

В статье рассматриваются отдельные подходы к оценке влияния инфляции на основные фонды компаний. Представлена функция для оценки влияния инфляции на коэффициент продолжительности основных фондов. В работе также предложен метод оценки основных фондов компаний с учетом коэффициента инфляции. Данный метод включает этапы приведения номинальной стоимости основных средств до уровня реальной инфляции, существенные финансово-хозяйственные действие, которые влияют на стоимость основных средств, а также сравнительный анализ функции упругости и определение приоритетных областей для повышения эффективности использования основного капитала. Метод протестирован с использованием материалов ОАО «Мосэнерго».

Ключевые слова: основные средства, инфляция, коэффициент продолжительности, рентабельность, эластичность, эффективность.

Kalubi R.D.M.

ORCID: 0000-0003-4016-0861, 3rd Year Postgraduate student, Peter the Great St. Petersburg Polytechnic University

IMPACT OF INFLATION ON THE ANALYSIS OF FIXED ASSETS

Abstract

This article deals with distinct approaches to the impact of inflation on the fixed assets of companies. It presents a function that evaluates the effects of inflation, on the coefficient of life of the fixed assets. It also proposes a method of evaluating fixed assets of the companies by taking into account the inflation factor. The method includes steps of bringing the nominal value of fixed assets to the levels of real inflation, substantial financial and economic activities that influence the cost of the fixed assets, a comparative analysis of the elasticity function and identification of the priority areas to increase the efficiency of use of fixed capital. The method was tested using the materials of OJSC “Mosenergo”.

Keywords: fixed assets, inflation, coefficient of life, profitability, elasticity, effectiveness.

Introduction

It ought to be noted that in economics there is no single, generally accepted approach to the determination of a criteria and indicators of the effectiveness of fixed capital. The Soviet Union for example used the extensive regulatory approach to assess the effectiveness of fixed assets [2, p.17]. The most important feature of this approach is to compare the relative performance of indicators of the fixed assets, such as capital-labor ratio, capital productivity, wear and tear factor, etc., with some different groups of equipment and industries. P.G. Bunich [3] examined in detail the contents of the normative approach to evaluating the effient use of the fixed assets.

Relevance: Long-term sustainable operations, the development of enterprises of different forms of ownership and types of economic activity are directly dependent on the nature of fixed assets. The effective use of the fixed assets has direct effects on the production of competitive products, profits and the profitability of the companies, meeting economic needs of various industries (owners of the means of production, the managers and employees).

The purpose and objectives of the paper: is to improve the methodological analysis of the company’s fixed assets. The main objectives identified in the paper include: - do critical analysis of the main approaches to the analysis of the fixed capital of enterprises; - develop a way of carrying out the analysis the analysis of fixed assets, using correlation and regression analysis techniques to study the elasticity production functions; - carry out testing of the developed method using OJSC "Mosenergo" materials.

Material and methods

In a free market economy, the regulatory approach to assessing the efficient use of the fixed assets in their purest form is problematic due to the complexity of determining the correct standards themselves. However, certain market regulatory modifications particularly by, S.M. Valitov and B.V. Bakeev compare the distinctive characteristics of using a company’s fixed assets not with legislative regulations, but with the average industry values [4, p.31; 12, p.92].

Modern international economics has a very popular approach where individual fixed capital performance indicators are linked with other potential performance indicators like human capital, financial growth indicators of companies, etc. This leads to the overall estimated contribution of the performance of fixed assets in ensuring the balanced development of companies (R. Kaplan, D. Norton [8] F. Herwig, W. Schmidt [17, p.11 - 15]).

In neo-institutional economics, traditional indicators which analyze the efficient use of fixed capital are complemented by studying transaction costs. Thus, according to R. Abrams, effective use of an enterprise’s fixed capital can be achieved in a minimum unit of transaction costs which are associated with purchases, use, repair and other operations [1, p.126]. I.A. Izakov [6, p.15] points out the need to consider transaction costs when analyzing the efficient use of fixed assets.

It ought to be noted that the effective use of fixed assets is directly influenced by inflation, proportions and their rates. Literature presents various points of view regarding the sort of the effect that inflation has on the effective use of fixed assets. The approach in which inflation has a clearly negative effect on the reproduction of the fixed assets of companies and their efficient use is dominant. G.U. Kasyanov points out very important two areas which distort the effect of inflation in the evaluation of the fixed assets of companies: Firstly, because of inflation the valuation of fixed assets which have a similar level of performance is significantly different; secondly, inflation reduces the real value of the depreciation of fixed assets which were acquired some time ago and they unnecessarily augment the tax base of the enterprise [7, p.34].

L.I. Chernikov connects inflation and augmenting market uncertainty, to reduction in long-term investment in the reproduction of fixed capital by companies [18, p.14]. According to G.B. Kleiner, high inflation increases the risks of unfair implementation of various types of contractual relationships, including contracts relating to the involvement of the fixed assets, their financing, using rent or lease [9, p.179].

Another group of researchers takes a distinct approach to the effect of inflation on the reproduction of fixed assets. N.I. Dolmatova in particular, indicates that with sustainable sources of financing, activities in the presence of complex science-based mechanisms of the renewal of fixed capital, inflation does not create significant obstacles for the organization and carrying out the reproduction process of fixed capital: under inflation, mechanisms for financing the replacement of fixed assets with respect to financial stability and efficiency of companies are adjusted [5, p.11;13, p.82; 14,p.90]. A similar view about the impact of inflation on the effective use of the fixed assets of a company is supported by K.S Fioktistov [16, p.35].

In my opinion, the impact of inflation on the reproduction of the fixed capital of companies is generally negative. Thus, high inflation significantly reduces the incentives to both accumulate capital as a whole, and to invest in fixed assets in particular, giving priority to short-term investments in working capital, securities for resale and foreign exchange. However, for some companies, an increase in inflation might be an incentive to improve the quality of asset management. Inflation has an insignificant impact on the reproduction of the fixed assets of companies that are financed through equity capital.

In general, the kind of impact that inflation has on certain indicators about the quality and effective use of particular fixed assets of a company can be determined using statistics.

It is worth mentioning that one of the most common indicators of the effective reproduction of the fixed assets of a company, industry or the economy in general is useful life, which is the ratio of the residual and initial value of fixed assets. Therefore, the higher the useful life (equal to one minus the coefficient of wear and tear, i.e. all things being equal), the higher the quality of fixed assets of a company, their productivity potential, and the ability to create funds for modern high technology products.

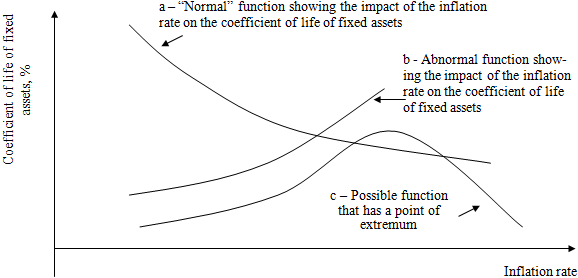

Fig.1 - Possible functions about the impact of the rate of inflation on the coefficient of life of fixed assets

Theoretically, there are several possible economic and statistical functions of how inflation affects the coefficient of life of fixed assets (Fig. 1):

- a) "Normal", a decreasing function, which shows that as inflation increases the coefficient of life of fixed assets of a company steadily decline. In an environment of high inflation, as a rule, it is more difficult to attract investment and long-term loans at an acceptable rate for particular businesses, this consequently slows down the process of the renewal of fixed capital and therefore increases their level of wear and tear.

- b) “Abnormal”, an increasing function which may be related to individual companies. Here, even a steady decrease of inflation in the economy does not entail an increase of the coefficient of life of fixed assets. This highlights the need for an integrated management system of fixed capital in companies (its inventory, sale of non-core assets, the rationalization of the composition and structure, etc.).

- c) This function has an extremum, which might indicate the presence of a relatively small optimum in terms of the reproduction of the fixed assets of a company owing to the inflation level in the economy. In some cases extremely low inflation caused by the drop in consumer demand can reduce the turnover of the company, decrease profitability, thereby reducing the possibility of raising equity capital for the renewal of fixed assets and consequently, reduce the coefficient of life of fixed assets.

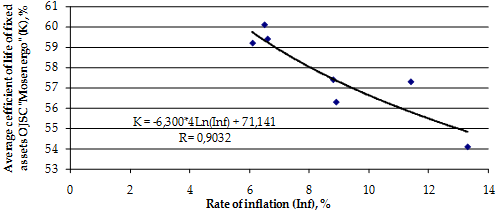

This technique will be tested on OJSC "Mosenergo" - one of the leading energy companies in the Russian Federation (Fig. 2).

Fig.2 - Economic and statistical function of the impact of inflation on the coefficient of life (2008 - 2014) (constructed by the author using the information contained in [11], [15])

As shown in Figure 2. The function of the effect of inflation on the average coefficient of life of fixed assets of OJSC "Mosenergo" is steadily decreasing, "normal." The Statistical representation of the built function shows the value of the correlation coefficient (R) close to one. In consequence, the reduction in macroeconomic parameters such as the inflation rate in the whole Russian economy is an essential external condition for augmenting the coefficient of life of the fixed assets of OJSC "Mosenergo", thereby increasing the effectiveness of their reproduction as a whole.

The paper proposes a method of assessing the effectiveness of the fixed assets of a company, taking into account the inflation factor. The following steps are involved in the procedure:

- Estimating the real residual value of the fixed assets of a company by adjusting the nominal residual value of the fixed assets at the inflation rate.

- Using economic and statistical functions to show the impact of the real value of fixed assets on the rate of change of a company's physical production (1) using management accounting data and the company's financial statements over a number of periods:

where V – is rate of change of real revenues from product sales (works, services);

OF – is the real residual value of fixed assets.

- Using economic and statistical functions to show the impact of the real value of fixed assets on product profitability (2):

where P - is the profitability of the company.

- Using economic and statistical functions to show the impact of the real value of the fixed assets on the index share of innovative products of the company in the overall structure of the issue (3):

where DI - is the share of innovative fixed assets in their overall structure

- Investigating functions that impact the real value of fixed assets is one of the most important indicators of company development, describing the level of business activity in the market, efficient production and innovation processes. Ideally, this type of function should be increasing and elastic, i.e., an increase in the real value of fixed assets should cause a rapid increase in the corresponding outcome of variables.

- Comprehensive assessment of the effective use of the fixed assets of the company can be carried out using the following formula:

Eff = (E (V) + E (P) + E (DI))*100% / 3 (4)

Where Eff - efficient use of the fixed assets of a company;

E – changes in the elasticity of the respective variable functions (1 - 3) depending on the changes in the real value of fixed assets.

Thus the elasticity of a specific period of time can be estimated by the following basic formula:

E = (dy / dx) * (x / y) (5)

where x, y - variable factors and results of functions;

dy / dx - the value of the derivative function y = f (x).

- Identification of the most important ways of improving the system of a company’s asset management based on comparative evaluation of elasticity. So, the least favorable situation is the insignificant or negative impact of elasticity on the real value of fixed assets on the corresponding performance indicators of the company:

- in the case where the smallest elasticity function V = f (OF), raises the level of use of fixed assets to intensify output, to rationalize the usage time of equipment, minimize downtime during its use;

- in the case where the smallest elasticity function R = f (OF), the highest priority is the rational management of the composition and structure of fixed assets which produce products with relatively higher added value (sales of non-core and non-performing assets, purchase of more equipment which produce more competitive products, including renting or leasing, etc.);

- in the case where the smallest elasticity 1`function DI = f (OF), the priority is to modernize the technical and technological structure of fixed assets, intensify research and development for the creation and implementation of innovative technologies and equipment.

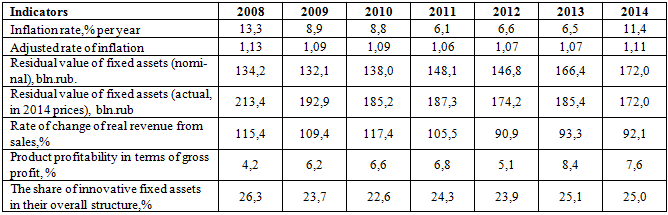

The technique was tested using the approved materials of OJSC "Mosenergo". Initial data for the calculation of the function showing the impact of the real value of fixed assets on the performance of the organization under study is shown in Table 1.

Table 1 - Initial data for the approbation of the proposed methodology of assessing the efficiency of fixed assets of a company (using the materials of OJSC "Mosenergo") [11], [15])

Based on the information provided in Table 1, the impact of the economic and statistical functions on the real residual value of fixed assets of OJSC "Mosenergo" is included in the performance methods and evaluation of elasticity functions.

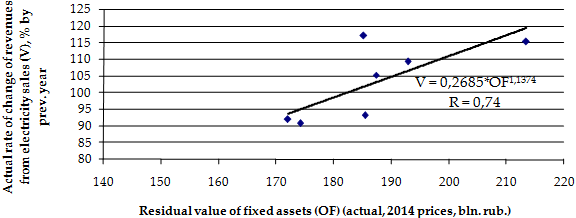

Fig.3 - Shows the real impact of the economic and statistical function of the residual value of fixed assets on the rate of change of actual revenues of OJSC "Mosenergo" (2008 - 2014)

The elasticity function represented in Fig.3, can be determined as follows:

E(V) = (0,32*OF0,13) * (OF/V) (6)

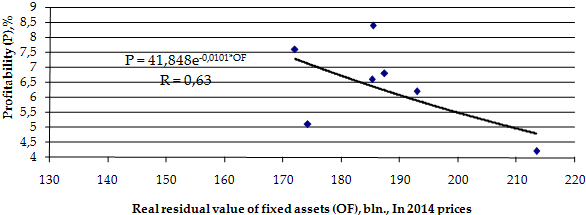

Fig.4 - shows the impact of the economic and statistical function of the actual residual value of fixed assets on the profitability of OJSC "Mosenergo" (2008 - 2014)

The elasticity function shown in Fig.4, can be determined as follows:

E(P) = (-0,42*e-0,01*OF) * (OF/P) (7)

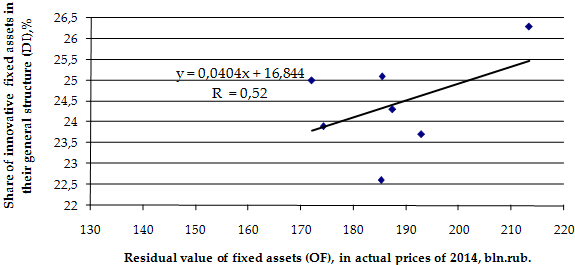

Fig.5 - Shows the impact of the economic and statistical function of the actual residual value of fixed assets on innovative fixed assets in the overall structure of fixed capital of OJSC "Mosenergo" (2008 - 2014)

The elasticity function shown in Fig.5, can be determined as follows:

E(DI) = 0,04*(OF / DI) (8)In accordance with the proposed method, we will evaluate the effectiveness of the use of fixed assets of OJSC "Mosenergo" (Table 2).

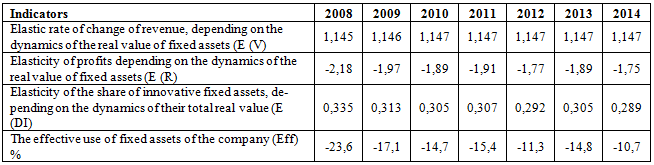

Table 2 - Evaluating the effective use of fixed assets by OJSC "Mosenergo”

As shown in Table 2, negative (-) elasticity shows the impact of the changes in the real value of the fixed assets of OJSC "Mosenergo" on its profitability. Negative elasticity offsets the positive impact of the real value of fixed assets on the rate of change of the organization's real revenue and innovative activities for the renovation of company equipment. In consequence, the most significant approach to increase the efficiency of fixed assets of OJSC "Mosenergo" is the intensification of measures to improve their technical and technological structure in order to increase their profitability (for example, by continuing the policy of integrated automation through management of fixed capital, optimize equipment placement, construction of new generating capacity, minimizing unsustainable downtime of equipment, elimination of non-core assets in the subsidiaries or sale them).

Scientific novelty: In general, the suggested method allows us to investigate the nature of the impact of the value of fixed assets of the company in terms of the factors of inflation to their real value, on key performance indicators of a business entity and to identify priority areas for modernizing the management of fixed capital. The necessary prerequisite for the representative use of this technique is the correctness and objectivity of official statistics estimating the level of inflation in the economy.

Conclusion

The developed method can be used for comparing the efficiency of fixed assets of a company for different periods of time and for a comparative evaluation of the effectiveness of fixed capital reproduction in several companies in the same industry, including different scales of industries.

Список литературы / References

- Abrams R. Entrepreneurship: A Real-World Approach. Redwood City: Planning Shop, 2012, 375 p.

- Александров Г.А., Павлов А.С. Обновление основных производственных фондов: интенсификация, эффективность, стимулы. М.: Экономика, 1986. 192 с. Alexandrov G. A., Pavlov A. S. Updating fixed production assets: intensification, efficiency, incentives. Moscow, Economics, 1986. 192 p. (rus)

- Бунич П.Г. Основные фонды социалистической промышленности. М.: Госпланиздат, 1960. 303 с. Bunich P. G., Fixed assets in socialistic industries. Moscow, Geoplanidae, 1960. 303 p. (rus)

- Валитов Ш.М., Бакеев Б.В. Индикативное планирование в экономических системах разного уровня. Казань: Из-во КГУ, 2003. 264 с. Valitov S. M., Bakeev B. V. Indicative planning in the economic systems of different levels. Kazan, KGU, 2003. 264 p.(rus)

- Долматова Н.И. Влияние инфляции на инвестиционный потенциал в современной экономике России: автореф. дис… канд. экон. наук. М., 2003. 24 с. Dolmatova N. I. Vliyanie inflyatsii na investitsionnyi potentsial v sovremennoy ekonomike Rossii. [The impact of inflation on investment potential in the modern economy of Russia]: avtoref. dis... cand.econ.sciences. Moscow, 2003. 24 p. (rus)

- Изаков И.А. Перераспределение прав собственности и его влияние на эффективность фирмы: институционально-экономический подход: автореф. дис… канд. экон. наук. Красноярск, 2014. 24 c. Isakov I. A. Pereraspredelenie prav sobstvennosti na effektivnost firmy: institutionalno – ekonomicheskiy podhod. [Redistribution of property rights and its impact on the efficiency of firms: institutional and economic approach]: avtoref. dis... cand.econ.sciences. Krasnojarsk, 2014. 24 p. (rus)

- Касьянова Г.Ю. Общероссийская классификация основных фондов и начисление амортизации. М.: Абак, 2015. 416 с. Kasyanova G. Y. All-Russian classification of fixed assets and depreciation charges. Moscow, Abacus, 2015. 416 p. (rus)

- Каплан Р., Нортон Д. Сбалансированная система показателей. От стратегии к действию. М.: Олимп-бизнес, 2013. 314 с. Kaplan R., Norton D. Balanced scorecard. From strategy to action. Moscow, Olympus-business, 2013. 314 p. (rus)

- Клейнер Г.Б. Стратегия предприятия. М.: Дело, 2008. 568 с. Kleiner G.B. Enterprise Moscow, Delo, 2008. 568 p. (rus)

- Лопатников Л.И. Экономико-математический словарь. М.: Дело, 2003. 520 с. Lopatnikov L. I. Economics and mathematics dictionary. Moscow, Delo, 2003. 520 p. (rus)

- Материалы ОАО “Мосэнерго”. URL: www.mosenergo.ru (дата обращения 20.12.2015). The materials of the OJSC “Mosenergo”. URL: http://www.mosenergo.ru/eng/catalog/5334.aspx (accessed on 20 December, 2015) (rus).

- Родионов Д.Г.Опыт жилищной реформы в странах центральной и восточной Европы. Инновации. 2007. №6. С.91-93.

- Родионов Д.Г., Кушнева О.А., Терентьева Н.А. Международный авторитет российской высшей школы: проблемы и пути решения. Инновации. 2013. №9(179). С.81-87.

- Родионов Д.Г., Кушнева О.А., Рудская И.А. Рейтинг университетов как инструмент в конкурентной борьбе на мировом рынке образовательных услуг. Инновации. 2013. №11(181). С.89-97.

- Российский статистический ежегодник. М.: Из-во Федеральной службы государственной статистики, 2015. 890 с. Russian statistical Yearbook. Moscow, Federal service of state statistics, 2015. 890 p. (rus)

- Фиоктистов К.С. Проблемы воспроизводства основного капитала // Вестник инвестиций и инноваций. №7. С.35 – 37. Feoktistov K. S. Problems of reproduction of fixed capita. Bulletin of investments and innovations. 2014. no. 7, pp. 35 – 37. (rus)

- Хервиг Ф., Шмидт В. Сбалансированная система показателей. М.: Финансы и статистика, 2007. 160 с. Herwig F., Schmidt V. Balanced system of indicators. Moscow, Finance and statistics, 2007. 160 p. (rus)

- Черникова Л.И. Воспроизводство основных фондов сельского хозяйства в условиях инфляции: автореф. дис… канд. экон. наук. Ставрополь, 2013. 24 с. Chernikova L..I. Vosproizvodstvo osnovnyh fondov selskogo hozyastva v usloviyah inflyatsii. [Reproduction of fixed assets of agriculture in terms of inflation]: avtoref. dis... cand econ.sciences. Stavropol, 2013. 24 p. (rus)

Список литературы на английском языке / References in English

- Abrams R. Entrepreneurship: A Real-World Approach / R. Abrams//. Redwood City: Planning Shop, 2012, 375 p.

- Alexandrov G. A., Pavlov A. S. [Updating fixed production assets: intensification, efficiency, incentives]/ G.A. Alexandrov., A.S. Pavlov//. Moscow, Economics, 1986. 192 p. [ In Russian]

- Bunich P. G., [Fixed assets in socialistic industries]/ P.G. Bunich//. Moscow, Geoplanidae, 1960. 303 p. [ In Russian]

- Valitov S. M., Bakeev B. V. [Indicative planning in the economic systems of different levels]/ S.M Valitov., B.V. Bakeev//. Kazan, KGU, 2003. 264 p.[ In Russian]

- Dolmatova N. I. Vliyanie inflyatsii na investitsionnyi potentsial v sovremennoy ekonomike Rossii. [The impact of inflation on investment potential in the modern economy of Russia]: / N.I. Dolmatova//. – Synopsis of PhD in Economics – M., 2003. -24 p. [ In Russian]

- Isakov I. A. Pereraspredelenie prav sobstvennosti na effektivnost firmy: institutionalno – ekonomicheskiy podhod. [Redistribution of property rights and its impact on the efficiency of firms: institutional and economic approach]:A. Isakov//. – Synopsis of PhD in Economics – K., 2014.-24 p. [ In Russian]

- Kasyanova G. Y. [All-Russian classification of fixed assets and depreciation charges]/ Y. Kasyanov//. M .: Abak, 2015. 416 p. [In Russian]

- Kaplan R.S., David P.N. The Balanced Scorecard: Translating Strategy into Action / R.S. Kaplan, P.N. David//. Boston: Harvard Business School Press, 1996.

- Kleiner G.B. [Enterprise strategy]/ G.B. Kleiner//. Moscow, Delo, 2008. 568 p. [ In Russian]

- Lopatnikov L. I. [Economics and mathematics dictionary]/ L.I. Lopatnikov//. Moscow, Delo, 2003. 520 p. [ In Russian]

- [The materials of the OJSC “Mosenergo”] [Electronic resource]. URL: http://www.mosenergo.ru/eng/catalog/5334.aspx (accessed: 20.12.2015). [ In Russian]

- Rodionov D.G. Opyt zhilishchnoy reformy v stranakh tsentral'noy i vostochnoy Yevropy [Testing housing reform in central and eastern Europe]/ D.G. Rodionov//. [Innovation] – 2007, №6. 91-93p. [In Russian]

- Rodionov D.G., Kushneva O.A., Terent'yeva N.A. Mezhdunarodnyy avtoritet rossiyskoy vysshey shkoly: problemy i puti resheniya [The international credibility of Russian higher education: problems and solutions]/ D.G. Rodionov, O.A. Kushneva, N.A. Terent'yeva//. Innovatsii. [Innovation] - 2013, №9(179). 81-87p. [In Russian]

- Rodionov D.G., Kushneva O.A., Rudskaya I.A. Reyting universitetov kak instrument v konkurentnoy bor'be na mirovom rynke obrazovatel'nykh uslug [University rankings as a tool to compete for educational services in the world market]/ D.G. Rodionov, O.A. Kushneva, I.A Rudskaya//. Innovatsii. [Innovation] – 2013, №11(181). 89-97p. [In Russian]

- Rossiyskiy statisticheskiy yezhegodnik. M .: Iz-vo Federal'noy sluzhby gosudarstvennoy statistiki [Russian statistical Yearbook. Moscow, Federal service of state statistics]. – M.: 2015. -890 p. [ In Russian]

- Feoktistov K. S. [Problems of reproduction of fixed capita. Bulletin of investments and innovations]/ K.S. Feoktistov//. 2014. no. 7, pp. 35 – 37. [ In Russian]

- Herwig F., Schmidt V. [Balanced system of indicators]/ F. Herwig., V.Schmidt//. Moscow, Finance and statistics, 2007. 160 p. [ In Russian]

- Chernikova L..I. Vosproizvodstvo osnovnyh fondov selskogo hozyastva v usloviyah inflyatsii. [Reproduction of fixed assets of agriculture in terms of inflation] / L.I. Chernikova//. – Synopsis of PhD in Economics – Stavropol, 2013. 24 p. [ In Russian]